Medical centres remain in strong demand.

The market for medical centres has remained strong through the COVID-19 pandemic and in some instances, there is evidence of strengthening. As a result of the pandemic, there has been a greater emphasis on the long term viability of tenant’s core business, which underpins the strength of the asset class. The medical industry is viewed as an essential service, with the industry demonstrating sound business fundamentals and strong cashflows characteristics, underpinning the tenant’s ability to pay rent. On this basis, we consider medical centres to be a defensive property asset class, which is well sought after in the current market.

The market for medical centres is driven by typical investment property market drivers, with investors seeking properties which offer sound fundamentals. This includes good physical characteristics in terms of location and quality nature of improvements as well as strong cash flow characteristics, including the calibre of tenants, WALE and sustainable passing income levels.

Whilst there has been a significant decline in the number of transactions since the start of the pandemic the demand for long leased property backed by well-regarded tenants is intensifying.

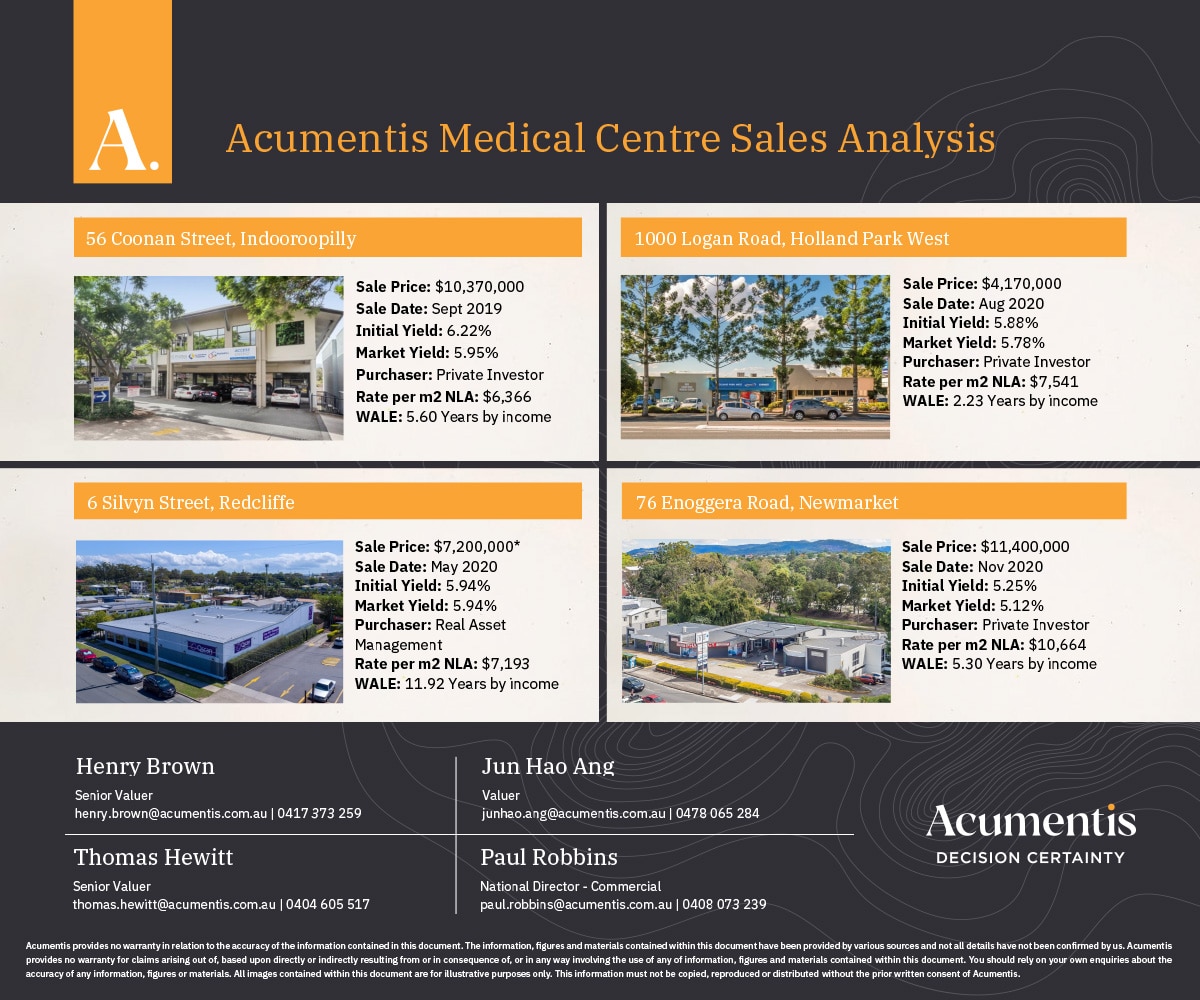

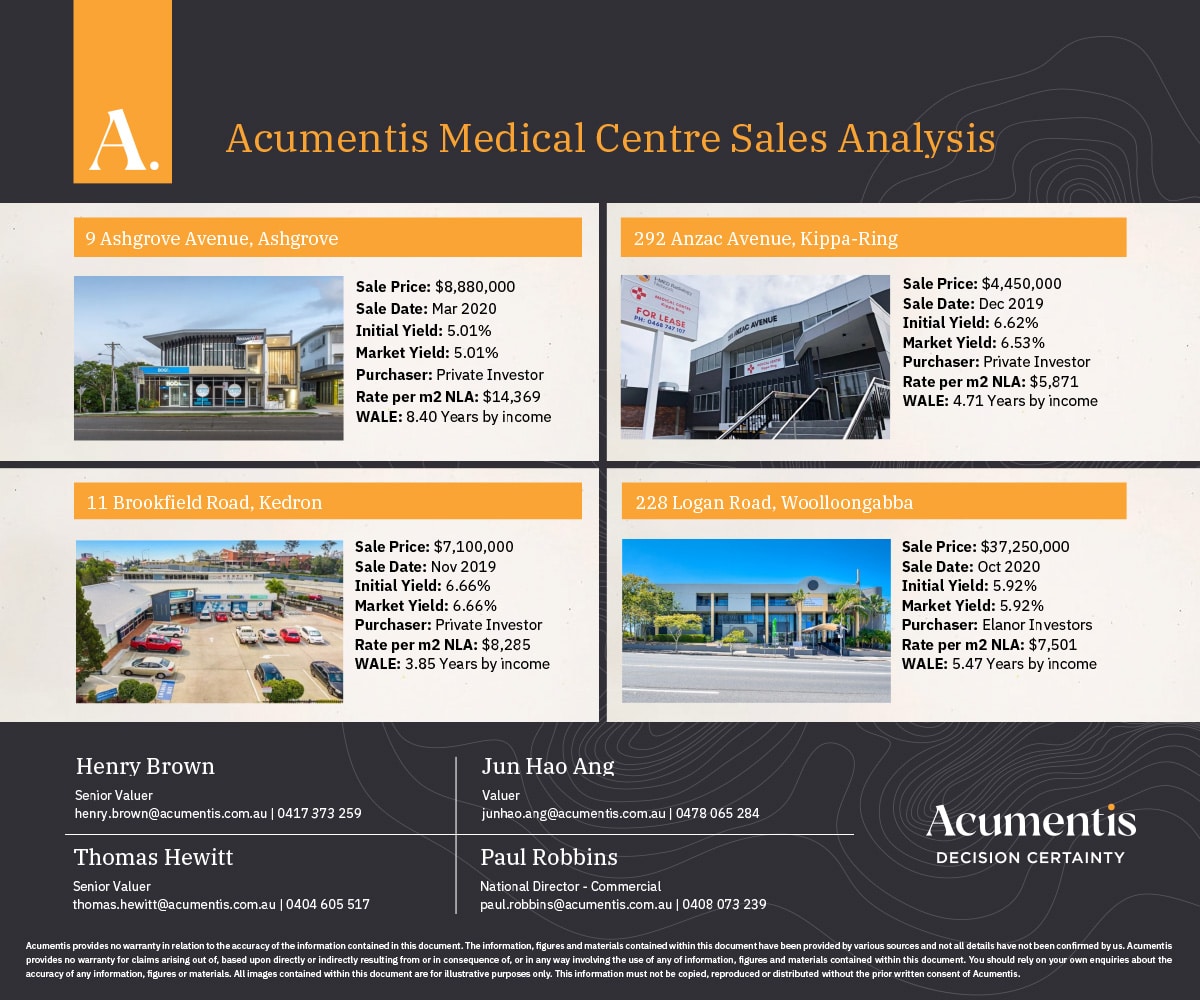

Click images to enlarge

Acumentis has witnessed yield compression across a range of asset classes and locations. Recent transactions (≤$50m) indicate a firming of yields by up to 75 basis points from 2019. With debt priced at historic lows, bank dividends drying up and term deposits at less than one per cent, we anticipate further demand from investors moving forward.

Considering the affordability of credit, we anticipate that the market will remain stable for prime assets with good investment fundamentals. The market for secondary assets will likely not improve until the impact of COVID-19 eases further and business confidence returns to other sectors of the economy.